Get Your Free Home Insurance Quote Now

Your home is your sanctuary, but unexpected events like fires, storms, or burglaries can disrupt your life. That’s where we come in.

Start protecting your home and possessions today with the right insurance coverage to help ensure your security.

Whether you’re a first-time homeowner or planning ahead, discover how Hilb Group can potentially help you save without compromising on quality.

Protect Your Home

"*" indicates required fields

Feel Confident in Your Protection

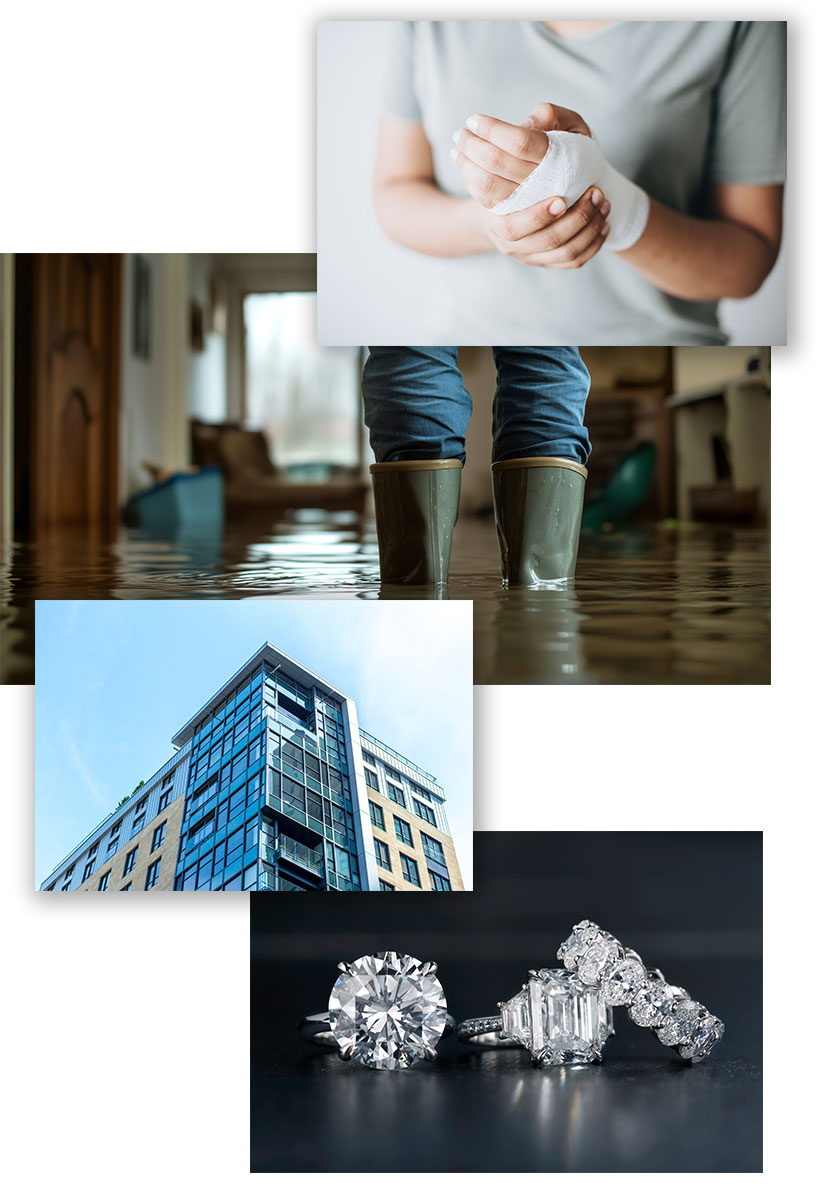

Common Homeowner's Challenges We Solve

Homeowners face countless challenges, from unpredictable weather to unexpected mishaps. Without the right coverage, you could be left with costly out-of-pocket expenses after a fire, storm, or accident.

But here’s the catch—not all insurance is built the same. Some policies leave gaps that can lead to stressful and expensive surprises, such as:- Rising insurance costs leaving you strapped for cash.

- Outdated policies that don’t provide enough protection.

- Confusion about what coverage you actually need.

- Limited options when purchasing directly from a single carrier.

How Hilb Group Is Different

What Does Our Comprehensive Homeowners Insurance Cover?

- Dwelling Coverage – Helps protect your home’s structure and pay for repair or rebuilding costs after a covered loss, such as vandalism, fire, windstorm, hail, hurricane, or water damage from plumbing or appliances.

- Other Structures – Covers detached structures on your property, such as garages, sheds, or fences.

- Personal Property Coverage – Covers theft or damage to personal belongings, such as furniture, electronics, and valuables. Depending on your policy, personal items may be repaired or replaced. Some policies may also include off-premises coverage for items stolen or damaged away from home.

- Liability Insurance – Shields you against lawsuits if someone is injured on your property or if you accidentally cause damage to someone else’s property. Liability insurance helps with paying legal fees and property damage claims if you are found responsible.

- Additional Living Expenses (ALE) – Pays for temporary housing and other living costs if your home becomes uninhabitable due to a covered event.

- Medical Payments – Covers minor medical expenses for guests injured on your property, regardless of fault.

- Loss of Use – Similar to ALE, it compensates for the loss of use of your home during repairs or rebuilding.

In short, since home insurance policies are designed to provide comprehensive protection for your property and personal belongings, it is important to insure your home for at least its estimated replacement cost. Keep in mind, Homeowners coverages may have deductibles and limits. Understanding these is important when filing a claim to make sure your repaired and replaced damaged property is covered.

Want More Peace of Mind?

Enhance Your Protection With Additional Coverage Options

Tailor your policy to your needs with extras like:

- Flood insurance for water damage in high-risk areas

- Umbrella policies for extra liability coverage

- Earthquake protection for seismic regions

- Valuable property add-ons for heirlooms, jewelry, or high-end electronics

- Specialized policies are also available, such as mobile home insurance for manufactured or mobile homes, condo insurance for condo owners (covering the interior of the unit), and renters insurance for tenants seeking to protect their personal property.

Bundle and Save More

Why stop at home insurance? Bundle your policies together to unlock insurance discounts! Our unique ability to bundle policies across multiple carriers can save you significantly without compromising on quality.

HOME + AUTO INSURANCE

HOME + LIFE INSURANCE

CUSTOM BUNDLES

See What Our Customers Are Saying

Secure Your Home Today

Your home deserves the best protection, and we’re here to make it easy and affordable. Don’t wait any longer to protect your home.

Join thousands of homeowners who trust Hilb Group to protect what they’ve worked so hard for.

Frequently Asked Questions

Homeowners insurance provides financial protection against damage to your home, belongings, and other liabilities.

We’re unbiased! We’ll compare options from multiple insurers to find you the coverage that best fits your needs and budget.

Absolutely! From basic protection to extras like Flood and Umbrella insurance, we’ll help you tailor your coverage to your specific concern.

Bundling policies (home, auto, and more) often unlocks discounts across the board. With Hilb, you can even bundle from different carriers for maximum savings and optimal coverage.

When it comes to protecting your home, understanding Homeowners insurance cost is essential for making smart financial decisions. The price you pay for a Homeowners policy can vary widely based on several factors, including the value of your property, your location, and the specific coverage options you select. For example, homes in areas prone to extreme weather or flooding may require additional Flood insurance, which can impact your overall property insurance cost.

Liability coverage is another important element, as it helps protect you from unexpected expenses like medical bills or legal fees if someone is injured on your property. Your mortgage lender may also require you to maintain a certain level of insurance coverage to protect their investment, so it’s important to factor this into your budget.

To get a clear picture of your home insurance cost, request a personalized Homeowners insurance quote from a trusted insurance advisor like Hilb Group. This will help you compare options and find a policy that offers the right financial protection for you. Also, remember to reviewing your coverage regularly so you’re not overpaying or underinsured as pricing fluctuates with market and weather related developments.

A thorough home inspection is a smart move for any homeowner looking to secure the best Homeowners insurance policy. Not only does a home inspection help identify potential risks—like frozen plumbing, water damage, or signs of theft—it also gives you and your insurance company a clear understanding of your property’s condition. This can directly impact both your coverage limits and the cost of your premium.

Here are two home inspection types that can save you money:

4-Point Inspections

A 4-point inspection focuses on your home’s four major systems—roof, electrical, plumbing, and HVAC—to verify they’re in good working order. Because many insurers want reassurance that these critical components aren’t near failure, a clean 4-point report can unlock policy eligibility or even discounts, especially on older homes.Wind Mitigation Inspections

In hurricane-prone areas, a wind mitigation inspection evaluates features that reduce wind damage: roof-to-wall connections, roof shape, opening protections (shutters or impact-resistant glass), and roof covering. Insurers often reward homes with strong wind-resistant upgrades through premium credits—sometimes up to 45% savings.

Working with a qualified inspector ensures that any hidden issues are brought to light before they become costly repairs. The inspection report can be a valuable tool when negotiating with your insurance company, helping you secure the right level of coverage for your unique needs. Some insurers even offer discounts for homes that have recently passed a professional inspection, which can help you save money on your premiums.

Beyond insurance, a home inspection can highlight areas where you can improve your home’s safety and resilience—like reinforcing your roof against extreme weather or upgrading security systems. These improvements not only help protect your home and personal property but also provide peace of mind knowing you’re prepared for whatever comes your way. Investing in a home inspection is a proactive step that helps protect your property, your budget, and your future.

Standard home insurance policies don’t extend to every peril. Common exclusions include:

Sinkhole damage (Florida has a separate sinkhole optional endorsement)

Sewer or drain backup (covered only with a water-backup endorsement)

Mold and algae growth (limited coverage)

Ordinance or Law losses (the extra cost to rebuild to current codes)

To fill these gaps, ask your advisor about adding endorsements, such as Sinkhole coverage, Sump-pump/Water-backup protection, mold remediation, and Ordinance or Law coverage. These extras can be surprisingly affordable and give you complete peace of mind.

Related Products

Private Client Group

Successful people need far more than an ‘insurance company’ to protect their assets.

Flood

Many people own homes in identified flood zones. They are typically required by their mortgage lenders to carry flood insurance, but most traditional homeowners policies do not cover this peril.

Umbrella

Umbrella Liability coverage guards against the unexpected